Report Overview

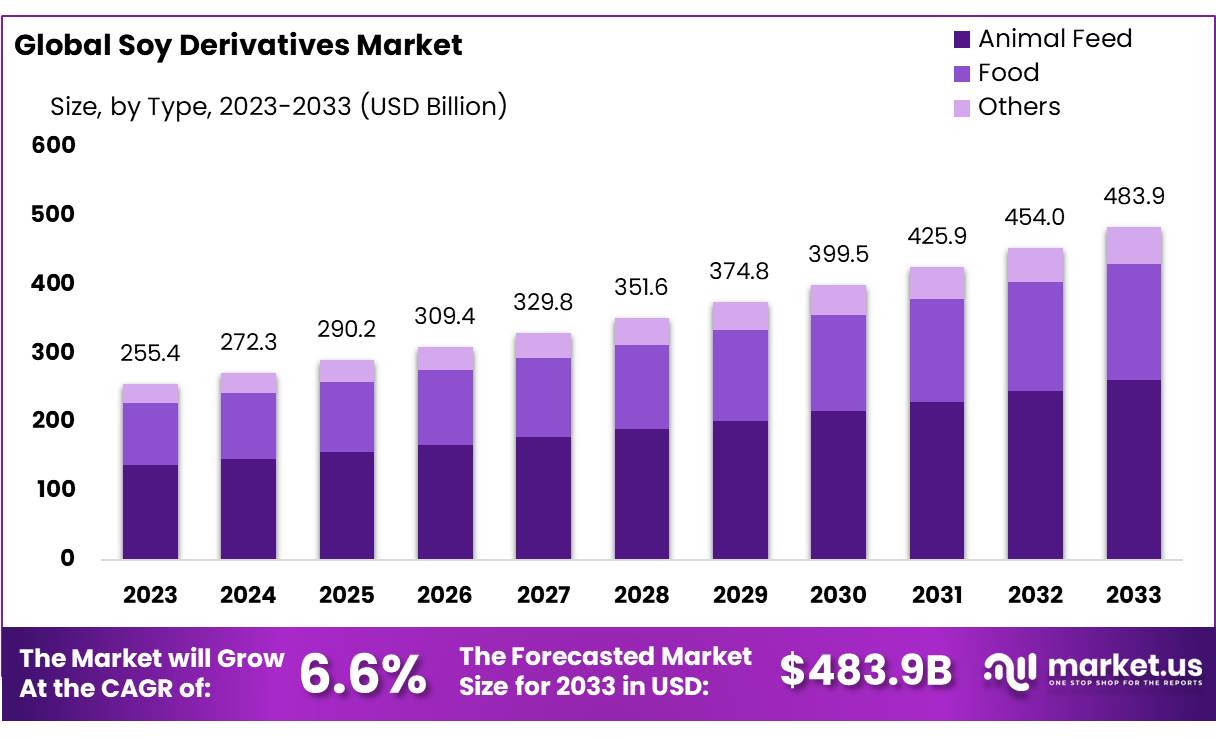

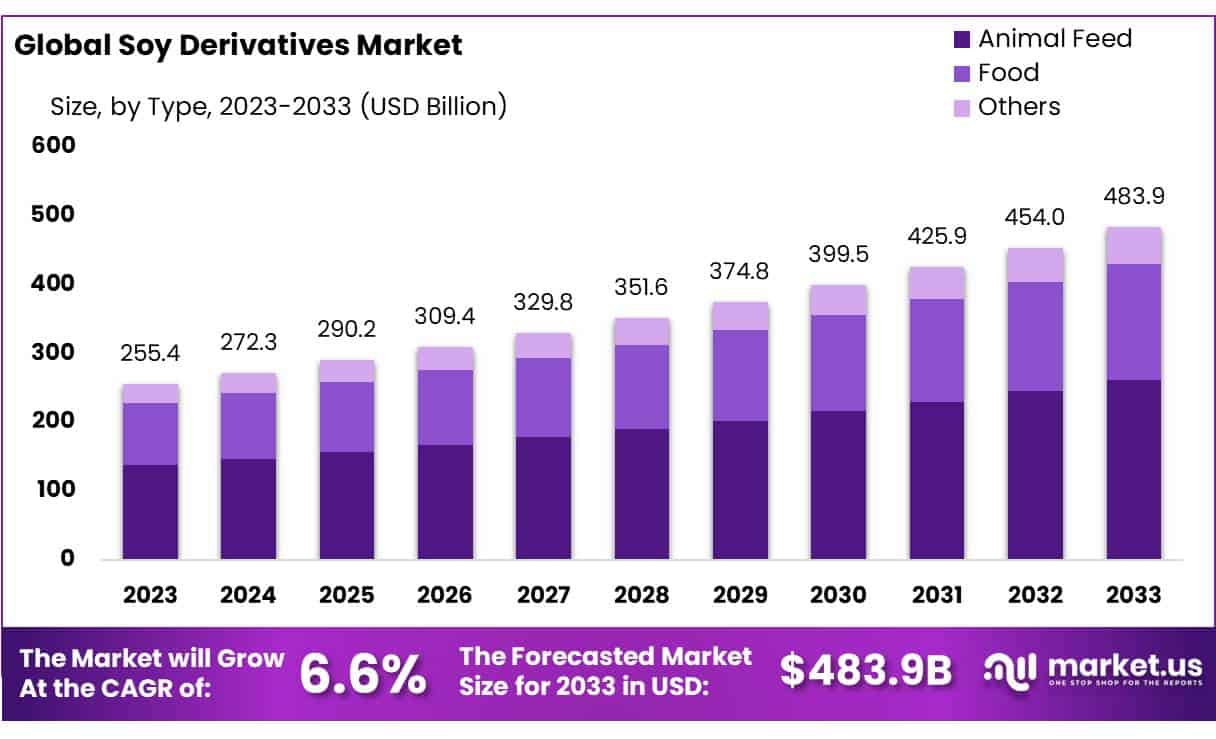

The Global Soy Derivatives Market size is expected to be worth around USD 483.9 Mn by 2033, from USD 255.4 Mn in 2023, growing at a CAGR of 6.6% during the forecast period from 2024 to 2033.

The global soy derivatives market is a critical segment of the agricultural and food industries, driven by the increasing utilization of soy as a versatile and sustainable ingredient. Soy derivatives, including soy protein, soy oil, soy lecithin, and soy isoflavones, are widely used across various sectors such as food and beverages, animal feed, pharmaceuticals, and personal care. The market’s growth reflects a combination of rising consumer demand for plant-based products, advances in food technology, and the expanding awareness of soy’s health benefits.

In 2023, the global soy derivatives market was estimated at approximately USD 240 billion, with a steady growth trajectory anticipated over the next decade. Soy oil dominates the segment, accounting for nearly 35% of the total market revenue due to its extensive application in cooking, biofuels, and industrial uses.

Soy protein is another significant segment, driven by the increasing adoption of plant-based diets. The United States, Brazil, and Argentina are key players in soybean production, collectively accounting for over 80% of global output. These regions are pivotal in ensuring the availability of raw materials, bolstered by advancements in agricultural practices and technologies.

The market’s growth is underpinned by several factors. First, the surging demand for plant-based protein in response to health and environmental concerns has significantly boosted soy protein consumption. In 2023, soy protein contributed to approximately 25% of global plant-based protein sales. Additionally, the increasing incorporation of soy derivatives in functional foods and dietary supplements has further driven demand, as soy is recognized for its role in promoting heart health, improving bone density, and managing cholesterol levels.

The animal feed sector is another key driver, with soymeal accounting for more than 70% of protein feed worldwide in 2023. The rising global population and growing demand for meat products indirectly fuel the market, as soy derivatives are a primary component in livestock feed.

Innovations in soy processing and derivative formulations are shaping market trends. For example, the development of non-GMO and organic soy derivatives caters to health-conscious consumers and addresses the growing demand for clean-label products. Furthermore, the expansion of soy derivatives in emerging economies, particularly in Asia-Pacific, is noteworthy. In 2024, China alone is expected to account for nearly 30% of global soy oil consumption, reflecting the region’s increasing reliance on soy-based products.

Opportunities lie in diversifying applications, such as using soy derivatives in biodegradable plastics and bio-based chemicals. Moreover, the growing interest in personalized nutrition presents avenues for innovation in soy-based functional foods.

The soy derivatives market showcases robust growth driven by evolving consumer preferences, technological advancements, and expanding applications across industries. Continued investment in research and sustainable practices will further unlock the potential of soy derivatives, making them an indispensable component of global agriculture and industry.

Key Takeaways

- Soy Derivatives Market size is expected to be worth around USD 483.9 Mn by 2033, from USD 255.4 Mn in 2023, growing at a CAGR of 6.6%.

- Animal Feed held a dominant market position, capturing more than a 54.3% share of the Soy Derivatives Market.

- Conventional held a dominant market position, capturing more than a 86.7% share of the Soy Derivatives Market.

- Soy Meal held a dominant market position, capturing more than a 46.6% share of the Soy Derivatives Market.

- Food & Beverage held a dominant market position, capturing more than a 48.1% share of the Soy Derivatives Market.

- Asia Pacific (APAC) region dominates, holding a 37.2% share with a market value of approximately USD 95 billion.

By Type Analysis

In 2023, Animal Feed held a dominant market position, capturing more than a 54.3% share of the Soy Derivatives Market. This segment has consistently led the market due to the growing demand for soy-based products in animal nutrition, driven by increasing livestock production globally. The rising awareness about the nutritional benefits of soymeal, a key soy derivative, has made it a staple in animal feed formulations. In 2024, this segment is expected to continue its strong performance, maintaining a significant share as farmers and livestock producers increasingly turn to cost-effective, high-protein alternatives for feeding animals.

The Food segment followed as the second-largest player in the market. In 2023, it accounted for a notable portion of the market share, thanks to the growing consumer preference for plant-based food products and the expanding vegan and vegetarian movements. Soy derivatives, including soy protein and soy lecithin, are widely used in processed foods, dairy alternatives, and meat substitutes. The demand for soy in food products is projected to grow steadily through 2024, with innovations in food technology and healthier food choices supporting this trend.

By Category Analysis

In 2023, Conventional held a dominant market position, capturing more than a 86.7% share of the Soy Derivatives Market. This segment’s strong market presence can be attributed to its wide availability and cost-effectiveness. Conventional soy derivatives, primarily produced using traditional farming practices, are extensively used in animal feed, food products, and industrial applications due to their affordable price point and large-scale production. As global demand for soy continues to rise, Conventional soy derivatives are expected to maintain their leading position through 2024, driven by their ability to meet the high-volume needs of various industries.

Organic segment accounted for a smaller portion of the market in 2023 but has shown notable growth. The demand for Organic soy derivatives has been steadily increasing as consumers and manufacturers alike become more conscious of sustainability and the environmental impact of production processes. Organic soybeans are grown without synthetic pesticides or fertilizers, which appeals to health-conscious consumers and those seeking natural or organic food products.

In 2024, the Organic segment is expected to continue growing, though at a slower pace compared to Conventional products, as more manufacturers adopt organic practices and as organic certification standards continue to evolve. While it is still a niche market, Organic soy derivatives are poised for further expansion, particularly within the health food sector and among environmentally aware consumers.

By Application Analysis

In 2023, Soy Meal held a dominant market position, capturing more than a 46.6% share of the Soy Derivatives Market. The popularity of soy meal is largely driven by its use as a high-protein feed ingredient in livestock and poultry farming. As the global demand for animal protein continues to rise, soy meal remains an essential part of animal nutrition due to its affordability and nutritional profile. In 2024, this segment is expected to maintain its leading position as the demand for sustainable and cost-effective animal feed remains strong.

Soy Oil followed as another key segment in the market, holding a significant share in 2023. Soy oil is widely used in the food industry for cooking and food processing, as well as in non-food sectors such as biodiesel production.

In recent years, soy oil’s popularity has been bolstered by the growing demand for plant-based cooking oils and the increasing use of biodiesel as an alternative fuel. This segment is projected to grow steadily through 2024, with rising consumer demand for plant-based oils and the continued shift toward sustainable energy sources.

Soy Milk, another important application, accounted for a notable share of the market in 2023, driven by the growing preference for plant-based dairy alternatives. As more consumers adopt vegan or lactose-free diets, the demand for soy milk has seen steady growth. In 2024, this segment is expected to continue its upward trajectory, supported by innovations in taste and texture that have made soy milk a popular choice among health-conscious consumers.

Soy Flour, while a smaller segment compared to Soy Meal and Soy Oil, also held a consistent market share in 2023. It is widely used in baking, food processing, and gluten-free products due to its nutritional benefits and ability to enhance food texture. In 2024, Soy Flour is expected to see moderate growth as more consumers and food manufacturers focus on gluten-free and high-protein dietary options.

By End-use Analysis

In 2023, Food & Beverage held a dominant market position, capturing more than a 48.1% share of the Soy Derivatives Market. This segment’s strength is largely driven by the increasing demand for plant-based food products, including meat substitutes, dairy alternatives, and health-focused snacks. Soy derivatives, such as soy protein and soy lecithin, are essential ingredients in many processed foods due to their versatility and nutritional value. As more consumers shift towards plant-based diets and healthier eating habits, the Food & Beverage segment is projected to continue its growth in 2024, with an increased focus on vegan, gluten-free, and organic product offerings.

Animal Feed, as the second-largest segment, accounted for a significant share of the market in 2023. The demand for soy meal as a high-protein animal feed ingredient remains strong, especially with the ongoing rise in livestock production worldwide. Soy derivatives are considered cost-effective and nutritionally balanced, making them a preferred choice in animal farming. In 2024, this segment is expected to maintain a substantial market share as global demand for animal-based products continues to grow, and the need for efficient, high-quality animal feed persists.

The Pharmaceuticals and Nutraceuticals segment also showed steady growth in 2023. Soy derivatives such as soy isoflavones and soy protein are increasingly being incorporated into supplements and functional foods due to their health benefits, including supporting heart health and hormonal balance. With the rising awareness of the benefits of plant-based ingredients for overall wellness, the Pharmaceuticals and Nutraceuticals segment is expected to experience moderate growth through 2024, as more consumers turn to soy-based supplements for their health needs.

The Personal Care segment, while smaller, has been growing steadily. Soy lecithin, soy oil, and other soy derivatives are used in a variety of personal care products, including skin creams, hair care formulations, and cosmetics, due to their moisturizing and emollient properties. As the demand for natural and organic beauty products increases, the Personal Care segment is expected to grow at a gradual pace through 2024, with soy derivatives becoming a more common ingredient in eco-friendly and sustainable beauty products.

Key Market Segments

By Type

By Category

By Application

- Soy Meal

- Soy Oil

- Soy Milk

- Soy Flour

- Others

By End-use

- Food & Beverage

- Animal Feed

- Pharmaceuticals and Nutraceuticals

- Personal Care

- Others

Drivers

Health and Nutritional Benefits Propel Demand for Soy Derivatives

A major driving factor behind the growth of the soy derivatives market is the recognized health and nutritional benefits of soy-based products. In recent years, there has been a significant increase in consumer awareness regarding the positive health impacts of including soy in the diet. Soy derivatives are highly valued for their high protein content, essential amino acids, and low levels of saturated fat, making them an excellent choice for individuals looking to improve their dietary habits.

As of 2023, the World Health Organization and various national health bodies have advocated for a higher intake of plant-based proteins to combat chronic diseases such as obesity, diabetes, and heart disease. Soy derivatives like soy milk, tofu, and soy protein isolates have been identified as heart-healthy food options by the American Heart Association due to their ability to lower blood cholesterol levels. This endorsement has encouraged more consumers to incorporate soy-based products into their daily diets.

The shift towards plant-based diets has been further accelerated by the global rise in lactose intolerance and milk allergies. Soy milk serves as a perfect alternative to dairy milk, offering similar nutritional benefits without the lactose, which has driven its popularity in both developed and developing markets. For instance, soy milk sales in the United States have seen consistent growth, with an increase of 6% in retail sales reported in 2024, highlighting its acceptance as a mainstream dairy alternative.

Furthermore, government initiatives aimed at promoting sustainable agriculture and food security have also supported the soy derivatives market. For example, the European Union has funded research and development projects to enhance soy cultivation within Europe to reduce dependency on soy imports and ensure a steady supply of this valuable crop. This support helps stabilize the market and ensures continuous growth in the demand for soy derivatives.

Additionally, the environmental benefits associated with growing soy, such as lower water usage and reduced greenhouse gas emissions compared to traditional livestock farming, resonate with the growing consumer ethos of environmental responsibility. This has not only spurred the demand among environmentally conscious consumers but also prompted food manufacturers to increase their offerings of soy-based products.

Restraints

Allergenic Concerns and Market Misconceptions Hinder Soy Derivatives Growth

A significant restraining factor impacting the growth of the soy derivatives market is the prevalent allergenic concerns associated with soy products. Soy is classified as one of the eight major food allergens, as identified by the U.S. Food and Drug Administration (FDA), which affects a notable segment of the global population. The potential allergic reactions can range from mild to severe, making it a cautious choice for many consumers, especially parents considering dietary options for children.

In 2023, the FDA reported that approximately 0.4% of American children have a soy allergy, with many of them not outgrowing it by adulthood. This prevalence of soy allergies contributes to consumer hesitation about integrating soy derivatives into daily diets, despite their known health benefits.

The mandatory allergen labeling laws in the United States and the European Union require clear indication of soy content on food packaging, which, while beneficial for consumer safety, also serves as a constant reminder of the potential health risks, thus dampening purchase enthusiasm among a wide audience.

Moreover, misconceptions and mixed messages about the health impacts of soy consumption add to the market’s challenges. Despite scientific studies supporting the beneficial aspects of soy, such as its potential role in lowering cholesterol and balancing hormones, there is still widespread skepticism. Myths about soy’s effects on hormonal balance and thyroid function continue to circulate, creating uncertainty and reluctance among potential consumers.

Government initiatives aimed at educating the public about the nutritional benefits and safe consumption levels of soy could help mitigate some of these concerns. However, the persistence of soy allergy issues and enduring myths likely will continue to act as barriers to the soy derivatives market’s full potential. Addressing these challenges requires ongoing efforts from both health authorities and industry leaders to provide clear, science-based information to the public to dispel myths and highlight the positive dietary role that soy derivatives can play.

Opportunity

Expansion into Emerging Markets Presents Major Growth Opportunities for Soy Derivatives

A significant growth opportunity for the soy derivatives market lies in its expansion into emerging markets, particularly in Asia, Africa, and Latin America. These regions are experiencing rapid urbanization, rising incomes, and an increasing awareness of health and wellness, which collectively create a fertile ground for the adoption of soy-based products. As local diets evolve and incorporate more diverse and nutritious ingredients, soy derivatives stand out due to their high protein content and health benefits.

In 2023, Asia accounted for a considerable increase in the consumption of soy derivatives, driven by changing dietary habits and the growing popularity of plant-based diets. Countries like China and India, with their large populations and rising middle-class consumers, are seeing a surge in demand for food products that offer health benefits without compromising on taste or nutritional value. The soy milk and soy oil segments, in particular, are expected to see robust growth rates in these markets due to their versatility and established presence in local cuisines.

Furthermore, government initiatives across these regions support the growth of the soy derivatives market by promoting agricultural development and food security. For example, several African nations have introduced programs to encourage soy cultivation as a means to boost their food production capacities and reduce protein malnutrition. These initiatives not only provide a stable supply of soybeans for local derivative production but also open up opportunities for market players to establish processing plants and distribution networks within these regions.

Moreover, the global shift towards sustainable and environmentally friendly products is particularly resonant in emerging markets, where the impacts of climate change are often more directly felt. Soy derivatives are viewed favorably in this light due to their lower environmental footprint compared to animal-derived proteins. This aspect is increasingly being marketed by companies looking to appeal to environmentally conscious consumers.

The potential for market growth in these regions is supported by the increasing involvement of international agencies and local governments in promoting nutritional education about the benefits of soy, which helps dispel myths and encourage the acceptance of soy products. As awareness grows and infrastructure improves, the demand for soy derivatives in emerging markets is expected to increase significantly, providing ample opportunities for market expansion and new product developments tailored to meet local tastes and dietary requirements.

Trends

Rising Popularity of Soy-Based Meat Alternatives Shapes Market Trends

A major trend in the soy derivatives market is the escalating popularity of soy-based meat alternatives. This trend is driven by a combination of environmental concerns, health consciousness, and ethical considerations regarding animal welfare. As consumers increasingly seek sustainable and healthier dietary options, soy-based products are gaining traction as viable substitutes for traditional meat.

In 2023, the global market for plant-based meat alternatives saw remarkable growth, with soy derivatives such as textured soy protein (TSP) and soy protein isolates playing pivotal roles. These ingredients are favored for their ability to mimic the texture and flavor of meat, making them ideal for creating a variety of meat-free products that appeal to both vegetarians and meat-eaters looking to reduce their meat consumption.

The rise in popularity of these soy-based alternatives is also bolstered by significant endorsements from health organizations and nutritional experts who highlight the benefits of reducing meat consumption and increasing plant-based intake for improving heart health and reducing the risk of chronic diseases. The American Dietetic Association, for instance, has published data supporting the nutritional adequacy of plant-based diets, which include soy as a key protein source.

Moreover, government initiatives are increasingly supporting the plant-based food sector as a strategy for sustainable development. For example, the European Union has funded research and innovation projects under the Horizon 2020 program that focus on enhancing plant protein extraction from soy, aiming to boost the production efficiency and quality of soy-based meat alternatives in the region.

This trend is supported by the growing availability and improving quality of soy-based products in supermarkets and restaurants worldwide. Food manufacturers are investing heavily in new product development and marketing to capitalize on the growing consumer demand for plant-based products. This includes expanding the range of available soy-based products from burgers and sausages to deli slices and ground meat substitutes, further integrating these alternatives into everyday eating habits.

Regional Analysis

In the global soy derivatives market, the Asia Pacific (APAC) region dominates, holding a 37.2% share with a market value of approximately USD 95 billion. This prominent position is largely due to the high consumption rates of soy products in countries like China, India, and Japan, where soy is a traditional staple. The region benefits from well-established soybean cultivation practices and a vast consumer base increasingly turning to soy-based products for health and dietary reasons.

North America also represents a significant portion of the market, driven by increasing consumer demand for plant-based diets and functional foods. The U.S. and Canada are seeing a surge in the adoption of soy derivatives, not only as meat alternatives but also in dairy-free products such as soy milk and tofu. This trend is supported by growing health consciousness and ethical concerns regarding animal welfare.

In Europe, the soy derivatives market is expanding steadily, supported by governmental and EU initiatives promoting sustainable agriculture and plant-based nutrition as part of their environmental and health strategies. European consumers are increasingly favoring soy derivatives as an alternative to meat and dairy products, which is pushing manufacturers to innovate and expand their soy-based product ranges.

Meanwhile, the Middle East & Africa and Latin America are experiencing slower growth in the soy derivatives market. However, these regions hold potential for future expansion due to rising health awareness and urbanization. Latin America, in particular, with its robust agricultural sector, is poised to increase its production and consumption of soy derivatives as local economies stabilize and demand for plant-based products grows.

Key Regions and Countries

- North America

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The soy derivatives market features a dynamic and competitive landscape with several key players driving innovation and market expansion. Among these, Archer Daniels Midland Company and Cargill, Incorporated are standout leaders. Both companies have extensive operations and robust product portfolios that include a wide range of soy derivatives such as soy proteins, oils, and flours.

Archer Daniels Midland Company, with its global supply chain and advanced processing capabilities, is pivotal in meeting the rising global demand for soy products. Cargill, on the other hand, leverages its vast network and expertise in food and agriculture to innovate in the product development and sustainability practices, particularly in the production of non-GMO and organic soy products.

Other significant players include Bunge Limited and Louis Dreyfus Company B.V., both of which are deeply entrenched in the agricultural commodities market. Bunge Limited is renowned for its integrated supply chain and focus on sustainable agricultural practices, which position it strongly in the soy derivatives market. Louis Dreyfus Company B.V. specializes in the efficient processing and distribution of agricultural goods, including soy derivatives, which are used across various sectors from food and beverage to animal feed.

Further contributing to the market are CHS Inc., Wilmar International Ltd., and DuPont Nutrition and Health. CHS Inc. plays a crucial role in supplying high-quality soy ingredients for food manufacturers and feed producers. Wilmar International Ltd. focuses on the Asian markets, capitalizing on the region’s vast demand for soy products.

DuPont Nutrition and Health brings a scientific approach to the market, offering soy-based ingredients that enhance nutritional content and product performance. Together, these companies not only influence market trends through their economic activities but also through their commitments to sustainability and health, shaping the future of the soy derivatives industry.

Top Key Players

- Archer Daniels Midland Company

- Cargill, Incorporated

- CHS Inc.

- Bunge Limited

- Louis Dreyfus Company B.V.

- Wilmar International Ltd.

- AG Processing Inc.

- DuPont Nutrition and Health

- Noble Group

- Tyson Foods

Recent Developments

In 2023, ADM continued to expand its influence and operations in the production of soy proteins, oils, and meals, essential components for a variety of industries including food, beverage, and animal feed.

In 2023, Cargill continued to focus on expanding its soy derivatives portfolio, which includes products like soy oils and soy proteins that are essential in food, feed, and industrial applications.

Leave a Reply